Stablecoins Are Reshaping Payments — and Putting Pressure on Fees

We've been paying a 3% convenience fee on commerce for 75 years and calling it normal. Stablecoins provide one of the largest margin-recapture opportunities in the global economy.

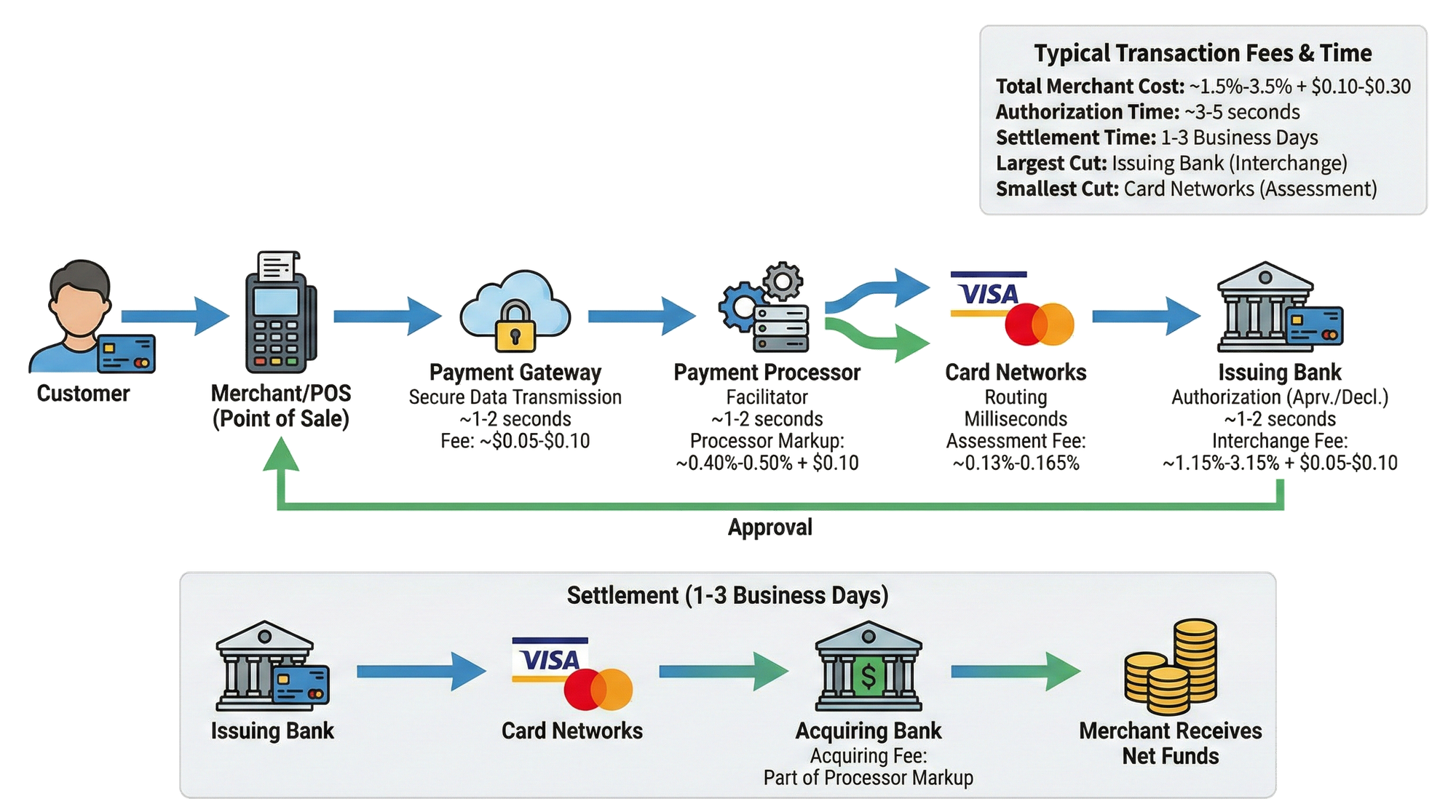

Every time you buy a $2 cup of coffee, about $0.30 vanishes into a chain of intermediaries — payment gateways, processors, card networks, issuing banks, acquiring banks — before $1.70 reaches the person who actually made it. That toll has been an unavoidable cost of modern commerce since the 1950s, when the first charge cards introduced a system of trust-through-middlemen that has survived every technological wave since: plastic, magnetic stripes, chips, NFC, mobile wallets. The interfaces changed. The economics didn't.

In 2025, U.S. merchants paid a record-breaking $187.2 billion (Source: MPC) in credit and debit card swipe fees, a 70% increase since the pandemic. For a retail giant like Amazon, this "circulatory tax" has likely scaled to between $7–11 billion annually. This is capital that doesn't improve the product, speed up delivery, or reduce prices; it simply evaporates into the financial plumbing of the global economy.

A stablecoin transaction on a modern blockchain accomplishes the same movement of value for under $0.01 and settles instantly. Not "authorized instantly, settled in two business days." Actually settled. That gap — from 2–3% down to fractions of a cent — represents one of the largest margin-recapture opportunities in the global economy.

And unlike previous fintech revolutions that merely reskinned the same rails, this overhauls the very idea of money.

The Scale of What's at Stake

The global payments industry is staggering in scope. In 2025, it handled approximately 3.6 trillion transactions, representing $2.0 quadrillion in value and generating $2.5 trillion in revenue (Source: McKinsey: The 2025 Global Payments Report). The United States alone processed $6.5 trillion in credit card payments and $4.4 trillion via debit. These are not small numbers being skimmed. This is the circulatory system of the global economy, and every transaction carries a tax.

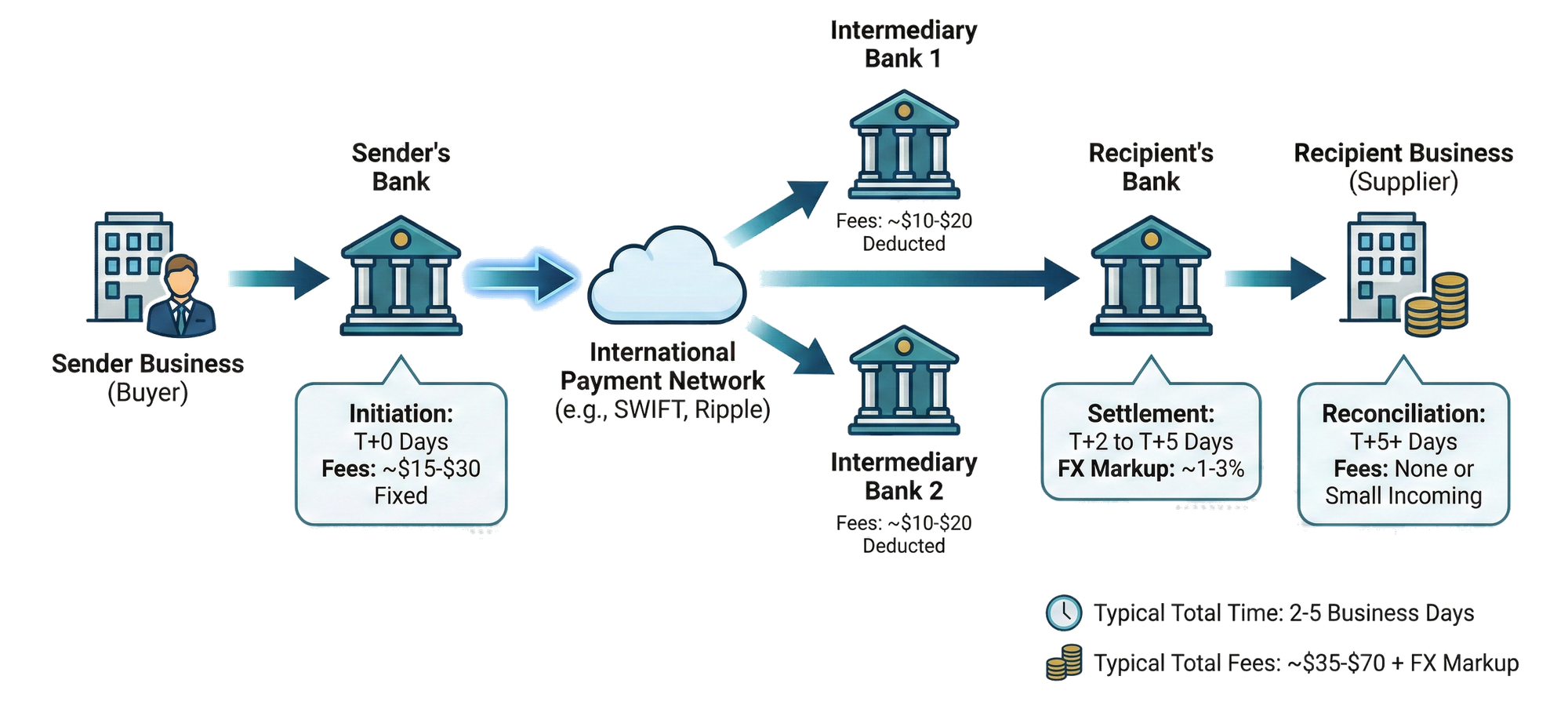

Other forms of payments are subject to arbitrarily high transaction fees as well. Sending money through traditional networks like SWIFT means contending with flat outbound fees of $25–50, hidden FX markups of 2–3% above mid-market rates, additional deductions from intermediary correspondent banks, and settlement times measured in days. Senders routinely face uncertain final delivery amounts, cash flow delays, and the administrative purgatory of tracing lost funds across borders.

These frictions are not bugs. They are features of a system designed around institutional trust and intermediation. Every hop in the chain exists because the previous architecture required a trusted party to verify, reconcile, and guarantee the transfer.

Stablecoins eliminate the need for most of those hops.

What's a Stablecoin?

A stablecoin is a digital token on a blockchain designed to maintain a 1:1 peg with a reference asset — most commonly the U.S. dollar. Unlike Bitcoin or Ethereum, which are volatile speculative assets, stablecoins act as programmable digital cash. They combine the high-speed, 24/7, borderless nature of blockchain with the price predictability of fiat currency.

The two dominant stablecoins — Tether's USDT and Circle's USDC — have a combined market capitalization exceeding $260 billion, with trading volume reaching $23 trillion in 2024 alone. Stablecoin supply has grown more than tenfold since 2020. In June 2025, the GENIUS Act was signed into U.S. law, establishing the first federal regulatory framework for payment stablecoins, requiring issuers to maintain 1:1 reserves in highly liquid assets like short-dated Treasuries. What was once a gray-area experiment now has a legal foundation.

A Structural Shift, Not an Incremental Improvement

This isn't just a minor optimization. It's a total re-architecture of money.:

| Feature | Traditional Payments | Stablecoins |

|---|---|---|

| Network | Closed, proprietary ledgers (Visa, SWIFT). Requires multiple intermediaries. | Open, public blockchains (Base, Solana). Shared global ledger. |

| Transaction Model | "Pull": Share card details to authorize deduction. High breach risk. | "Push": Cryptographically send exact amount. No sensitive data shared. |

| Intermediaries | 5+ (Gateway, Processor, Network, Issuing & Acquiring Banks). | Minimal (Sender Wallet → Blockchain → Receiver Wallet). |

| Settlement | T+1 or T+2 days. Batched processing; closed weekends. | Instant (milliseconds). 24/7/365 finality. |

| Merchant Fees | 1.5%–3.5% + $0.10–$0.30 per transaction. | ~$0.001–$0.01 per transaction. |

| Micropayments | Unviable. Fixed minimum fees erase profit on small items. | Highly viable. Sub-cent fees enable profitable micro-transactions. |

| Programmability | Rigid. Requires manual backend reconciliation for taxes, tips, and splits. | Native. Smart contracts instantly auto-route funds at the point of sale. |

| Cross-Border | Slow (days) and expensive (SWIFT). High FX spreads and wire fees. | Globally native. Same speed and cost as a local transaction. |

| Fraud Model | Centralized data storage creates honeypots. High chargeback risk. | Cryptographic finality. No card numbers to steal; immutable transfers. |

| Treasury Yield | Idle merchant funds sit in checking accounts earning 0%. | Funds can instantly route to yield-bearing tokenized assets (e.g., ~4.5% APY). |

The fundamental shift is from a pull-based system of shared secrets (your 16-digit card number, passed through five intermediaries) to a push-based system of cryptographic proof.

That single architectural change collapses the intermediary stack, eliminates settlement delay, and destroys the fee model that extracts $187 billion a year from American merchants alone.

The Evidence Is No Longer Theoretical

McKinsey and Artemis Analytics estimate that actual stablecoin payment volume (filtering out trading activity) hit $390 billion annually as of late 2025 — more than doubling from 2024. B2B payments dominate at roughly 60% of that volume, with a 733% year-over-year increase. Stablecoin-linked card spending grew 673% to $4.5 billion in 2025.

Visa's on-chain stablecoin settlement for card issuers reached a $3.5 billion annual run-rate by late 2025. PayPal's Pay with Crypto converts wallet balances into merchant payouts, targeting cross-border fee reduction. Stripe acquired stablecoin infrastructure company Bridge for $1.1 billion. Circle unveiled a new blockchain (Arc) with sub-second finality and transaction fees paid in USDC.

The interface stays familiar: tap, pay, done. But behind the curtain, stablecoins are already replacing legacy settlement. And this is just the opening act. The technology enables something far more fundamental — full self-custody and peer-to-peer value transfer without a single intermediary in between.

A Different Model Entirely

Traditional banking operates on a financial intermediary model: banks accept deposits, pool that capital, and leverage it through lending and investment. They then return a fraction of the yield to depositors as interest. The Net Interest Margin (NIM)—essentially the difference between the interest income a bank earns on its assets (like loans) and the interest expense it pays out to depositors—is crucial. Typically ranging around 3–3.5 percentage points, this margin covers real costs such as regulatory compliance, FDIC insurance premiums, credit risk management, branch infrastructure, and fraud resolution, while also generating profit.

In a self-custodied wallet, assets remain on a decentralized ledger under the user's direct control. The wallet architecture consists of an asymmetric key pair: a public key that functions as a receivable address, and a private key — stored locally or in a hardware device — that cryptographically authorizes all outbound transactions. The transaction model is push-based: the user signs a transaction specifying the exact amount and destination, eliminating the need to share reusable credentials.

The yield mechanism operates through decentralized lending protocols — smart contracts deployed on public blockchains that programmatically match lenders with borrowers.

Remarkably, Real World Asset (RWA) protocols now bring sovereign debt yields directly to the blockchain. A leading example is BlackRock’s BUIDL fund, which tokenizes U.S. Treasuries to pass a current yield of approximately 4.5% directly to token holders. By replacing physical infrastructure and heavy regulatory overhead with smart contracts, these protocols offer higher capital efficiency and 24/7 liquidity; however, they also swap legacy safety nets like FDIC insurance for modern technical risks like smart contract vulnerabilities, oracle manipulation, governance attacks and liquidity crises.

Here are leading alternatives to BlackRock’s BUIDL:

| Issuer / Token | Underlying Assets | Target Audience | Key Differentiator |

|---|---|---|---|

| Franklin Templeton (BENJI) | U.S. Gov Securities, Cash, Repo | Retail & Institutional | Multi-chain (Stellar, Polygon, Arbitrum, etc.); open to retail investors. |

| Ondo Finance (OUSG / USDY) | Short-term U.S. Treasuries | Institutional & Crypto-native | Industry standard for DeFi composability and lending protocol integration. |

| Superstate (USTB) | Short-duration U.S. Treasuries | Institutional & Crypto Funds | Programmable collateral optimized for crypto market makers; founded by Compound's creator. |

| Hashnote (USYC) | T-bills & Reverse Repo | Institutional Traders | Seamless USDC mint/redeem integration for rapid collateral mobility. |

| WisdomTree (WTGXX) | Government Money Market | Retail & Institutional | SEC-registered mutual fund distributed via their own consumer app. |

| JPMorgan (Onyx) | Tokenized Money Market | Institutional Only | Institutional-grade yield built on Tier-1 banking infrastructure. |

The model is viable and improving, but characterizing it as a risk-free alternative to banking would be inaccurate.

What's Holding It Back

Regulatory complexity is real, even post-GENIUS Act: The law establishes a framework, but implementation is pending. Federal regulators (OCC, Fed, FDIC, NCUA) have until December 2026 to issue final rules. States must demonstrate "substantially similar" oversight to approve their own issuers. The interest-bearing stablecoin debate remains politically charged, with bank lobbies pushing to restrict yield features that could compete with deposits.

Digital Asset Market Clarity Act: This legislation is designed to establish a comprehensive federal regulatory framework for the cryptocurrency and digital asset industry. The Clarity act has to walk a fine line keeping all the stakeholders aligned: banks, regulators, crypto bros..

| Stakeholder | The Core Problem / Challenge |

|---|---|

| Blockchain Developers & Crypto Startups | Crippling regulatory ambiguity and the threat of sudden enforcement actions have stifled innovation and driven many founders offshore. |

| SEC & CFTC (Federal Regulators) | A persistent jurisdictional dispute over whether specific digital assets should be treated as securities (SEC) or commodities (CFTC). |

| Traditional Banks & Institutions | Severe legal uncertainty has prevented them from safely offering crypto custody, trading, or stablecoin services to their clients. |

| Everyday Investors & Consumers | Fragmented oversight and regulatory loopholes leave the public vulnerable to market manipulation, fraud, and catastrophic exchange collapses. |

| Crypto Exchanges & Intermediaries | A lack of practical, lawful registration pathways to operate in the U.S. without facing overlapping or conflicting agency rules. |

| State Securities Regulators (e.g., NASAA) | Concerns that sweeping federal classifications might preempt state laws, limiting their ability to prosecute local crypto scams. |

A reconciled House-Senate package reaches the floor sometime in spring or early summer 2026. With strong crypto PAC spending, Trump administration priority, and broad (though not universal) bipartisan support, the odds of eventual passage are high — but the final text on stablecoin inducements, state preemption, and DeFi safe harbors will determine how “pro-innovation” the law actually is.

Merchant adoption remains indirect: Direct stablecoin acceptance at point-of-sale is still rare. Compliance burdens (AML/KYC), the absence of chargeback mechanisms consumers rely on, and immature merchant tooling all create friction. The practical path forward — and the one Visa and Stripe are betting on — is stablecoin settlement behind the existing card interface, not in place of it.

De-peg risk and reserve transparency: Tether's reserve composition has faced persistent scrutiny. The GENIUS Act addresses this by requiring 1:1 backing with highly liquid U.S. government securities, but enforcement mechanisms are still being built. The interdependence between stablecoin reserves and the Treasury market is growing in both directions — a development that regulators are watching closely.

Consumer protection gaps: Blockchain transactions are immutable. There's no "call your bank" recourse for erroneous transfers. Dispute resolution must be rebuilt at the application layer, and those systems are nascent.

Alternatives: For consumers, credit cards charge no transaction fees, offer 1–3% cash back, include fraud insurance, and provide charge-back rights — the 3% interchange cost is borne entirely by merchants, giving consumers no incentive to switch. For domestic transactions, FedNow already delivers instant, 24/7 settlement at a fraction of a cent with no blockchain required.

What Comes Next

As someone who runs technology at a bank, I understand the mechanics on both sides of this equation — the legacy infrastructure that still works, and the emerging rails that threaten to make parts of it obsolete. Interchange revenue, float income, wire fees — these are real economics that fund real operations across the industry. But intellectual honesty demands acknowledging that the most profitable layer of the payments stack is also the most vulnerable.

The transition won't be a sudden flip. It will be a layered migration — stablecoins quietly replacing settlement plumbing underneath interfaces that still look and feel like the card swipes and checkout screens consumers already trust. But as payment costs compress toward zero, the business models sitting on top will have to evolve. Incumbents will scramble to monetize in new ways: taking a cut of stablecoin reserve yield, selling fraud detection and compliance tooling as standalone services, unbundling the credit-rewards-protection bundle that has been quietly subsidized by interchange for decades.

The deeper disruption, though, won't come from incumbents adapting. It will come from startups that couldn't be possible with the old rails at all. When every transaction is free, instant, and borderless by default, entirely new categories of commerce become viable — micropayment-funded content, machine-to-machine settlement, real-time revenue splitting across global supply chains, payroll that streams by the minute instead of arriving biweekly.

The $187.2 billion question isn't whether stablecoins will reshape payments. It's whether the institutions currently collecting those fees will be the ones building the next architecture — or the ones being routed around.

Appendix: Payment Rail Comparison

| Payment Rail | Estimated Cost | Settlement Speed | Notes |

|---|---|---|---|

| Standard ACH | $0.00–$0.50 | 1–3 business days | Batch processing. No weekends or holidays. |

| Domestic Wire | $15–$35 | Hours (same day) | Final and irrevocable. High-value only. |

| SWIFT (International) | $30–$50+ | 1–5 business days | Multiple correspondent banks take a cut. |

| Credit Cards (Visa/MC) | 1.5%–3.5% + flat fee | Auth instant / settle 1–2 days | High fees subsidize rewards, fraud protection, chargebacks. |

| RTP & FedNow | Fractions of a cent | Instant (seconds) | 24/7/365. Still rolling out across U.S. banks. |

| Stablecoins (L2 & Modern L1) | < $0.01 | Instant (seconds) | Globally native, 24/7, and programmable. Eliminates the intermediary stack. |

Data Citations & Sources

| Source Organization | Report Title / Data Set | Year of Publication | Data Portal / Link |

|---|---|---|---|

| Nacha | ACH Network Volume Statistics (2005–2025) | 2026 | Nacha Network Statistics |

| SWIFT | Annual Review / FIN Traffic Figures | 2025 | SWIFT Traffic Figures |

| Bank for International Settlements (BIS) | Red Book Statistics on Payment Systems | 2025 | BIS Payment Statistics |

| The Nilson Report | Global Card Performance History (Issues 850–1301) | 2025 | The Nilson Report Archive |

| Visa Inc. | Annual Global Volume Summaries | 2025 | Visa Investor Relations |

| The Clearing House | RTP Network Quarterly Performance Reports | 2025 | TCH RTP Network |

| Federal Reserve Financial Services | FedNow Adoption and Volume Metrics | 2026 | FedNow Explorer |

| McKinsey & Company | Global Payments Report: The Shift to Programmable Settlement | 2026 | McKinsey Financial Services |

| World Economic Forum / Allium | Stablecoin Surge: Reserve-backed Cryptocurrencies on the Rise | 2025 | WEF Publications / Allium Data |

| Artemis Analytics / TRM Labs | 2025–2026 Crypto Adoption and Stablecoin Usage Report | 2026 | Artemis Terminal / TRM Insights |