Crypto Trends (Late 2021)

Decentralized public blockchain applications are thriving, growing in breadth, maturity, and volume. They have graduated from being a speculative asset to a platform that is able to compete directly with established financial services businesses.

This post will survey key concepts and trends in the cryptocurrency/blockchain space as of late 2021.

Key Trends

- Bitcoin is becoming ever more mainstream: SEC approved a Bitcoin ProShares ETF in October 2021, El Salvador’s adopted it as legal tender in June 2021 and established Hedge Funds are deep in crypto. Bitcoin has shown resilience despite the Chinese clampdown, and it has emerged as a hedge for inflation.

- Central Bank Digital Currencies (CBDCs) launching in Europe and Asia are likely to normalize blockchain use further and encourage widespread adoption in payment networks, banking, and social networks.

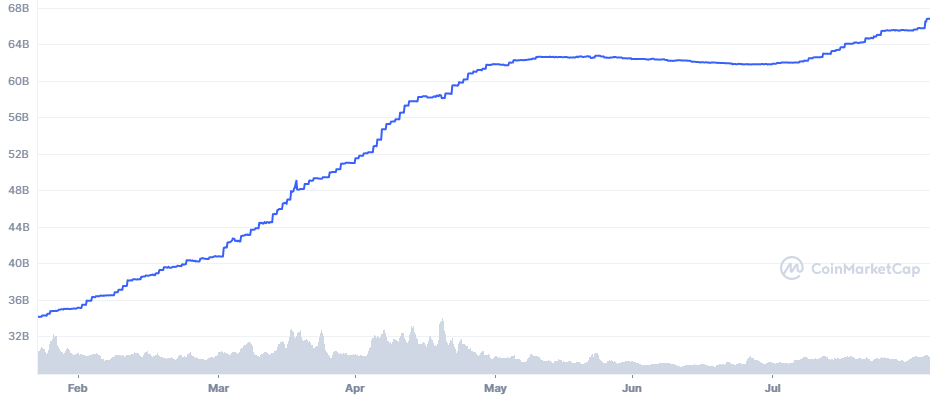

- NFT and DeFi applications are growing rapidly. The DeFi market grew from $700 million in December 2019 to around $80 billion in late 2021.

- Decentralized finance (DeFi) applications offer substantially greater financial returns than traditional institutions. They likely will present an interesting alternative to traditional financial businesses like banks.

- Centralized finance (CeFi) institutions such as Nexo allow a seamless transition between crypto and fiat currencies, including borrowing in fiat cash against crypto collateral. They have been bridging the gap to mainstream consumers, much like Coinbase.

- In the US, new crypto regulations are likely coming. These will probably focus on improving tax compliance, and greater oversight of stablecoins. But challenging topics like AML compliance remain to be solved.

- Decentralized web (or Web 3.0) is a new stack of technologies for the development of decentralized web applications that are hosted on the blockchain network. These technologies include blockchain as a trust verification mechanism, privacy-preserving and interoperability protocols, decentralized infrastructure and application platforms, decentralized identity, and support for applications like decentralized finance. These will eventually realize the vision of a decentralized web.

- Blockchains are migrating from the proof-of-work as a way to validate the integrity of their blockchain, to a more energy-efficient method called proof-of-stake. Eth2 is an ongoing upgrade to the Ethereum network that will utilize proof-of-stake to improve environmental footprint and transaction volume.

Crypto: Beyond a Store of Value

Early cryptocurrencies such as Bitcoin offered a medium of exchange, a unit of account, and a store of value. Modern blockchains act more like distributed computers that can execute programs and store their data.

Ethereum 2.0

Ethereum 2.0 also known as eth2 or Serenity, is a complete rewrite of the Ethereum protocol. It is designed to address some of the original limitations of Ethereum — in particular, limited throughput due to the proof of work consensus algorithm that validates transactions (just 15 to 45 transactions per second), as well as the costs of performing a transaction (In November 2021, it is approaching $6 USD.)

Ethereum 2.0 sets out the transition to a proof of stake (PoS) model that replaces the original proof of work mining with entities who “stake” or commit for the chance to validate transactions. Stakers holding a minimum of 32 ETH can earn interest on the amount of stake they deposit.

The upgraded network will support 100,000 transactions per second.

It is being released in roughly three phases:

- Phase 0: The beacon chain. Launched on 1 December 2020. This is the core chain that makes sure the shards across the network are kept in sync. It achieves this using validator.

- Phase 1: The shard chains. Expected 2022. Ethereum’s data and transactions will be run on shard chains. These are proof-of-stake blockchains that use validators to confirm transactions, create blocks, and communicate with the beacon chain.

- Phase 1.5: The legacy Ethereum chain becomes a shard on the new Ethereum blockchain. Expected 2022. In this phase, the legacy Ethereum network will transition to a proof-of-stake network and be connected to the main Ethereum 2 chain.

- Phase 2: Shards fully functioning. Expected 2022. The shard chains will be fully functioning and able to communicate with each other and run smart contracts.

Existing ETH tokens will be automatically accessible to the Ethereum 2 chain.

Stablecoins

Stablecoins are blockchain-issued cryptocurrencies designed for stability by being pegged to a specific value. The most popular stablecoins today are centralized and collateralized by pegged fiat currencies or assets held in reserve. Other decentralized stablecoins leverage crypto assets as collateral and the stablecoin is overcollateralized to maintain stability with volatile cryptocurrencies. Noncollateralized stablecoins are decentralized, and price stability is based on an algorithm.

Central banks and traditional financial services companies may be caught off guard by the growing popularity of stablecoins and miss new revenue opportunities that threaten legacy businesses. The Fed has been working with banks to decrease the time it takes people to receive money in their accounts. Stablecoins address this problem, since the tokens can be transferred quickly, rather than having to wait for any underlying dollars to hit someone’s account. Stablecoins can undermine existing business models and change the way users interact with financial systems and engage in business.

The largest stablecoin in circulation today is Tether (USDT), with around $70B in circulation in October 2021. Tether’s market cap in March 2021 grew past $40 billion, representing a tenfold growth in over 12 months.

Tether is facing increasing scrutiny from regulators. It was fined $41M by US regulators in October 2021 for misleading investors by claiming the token was fully backed at all times by US dollars.

Greater regulatory oversights of stablecoins in general, is very likely in the near future.

Decentralized Applications (dApps) and Distributed Finance (DeFi)

dApps are decentralized applications that run on the blockchain. Unlike regular apps, decentralized apps—as the name suggests—are built atop the decentralized infrastructure of peer-to-peer networks such as blockchains. That means no one entity or person has control of a dApp. Instead, it is secured by an infrastructure of nodes and crypto tokens. Because of this, dApps benefit from censorship resistance—with no single controlling entity, it is almost impossible for a government or individual to take control of the network and shut it down.

Their decentralized nature also means that they’re unlikely to suffer from downtime. In 2021, when a Bitcoin price crash caused trading volumes on crypto exchanges to surge, many centralized exchanges went down, while decentralized exchanges (DEXs) continued to run as normal.

DeFi refers specifically to finance-related dApps. DeFi eliminates the intermediaries and supports trustless, transparent, and immutable transactions between anonymous parties. When compared to centralized financial (CeFi), DeFi lowers transaction costs and improves process efficiencies. Based on open-source protocols, developers assemble financial primitives into reusable transformational applications that are not feasible using CeFi.

Lending and Borrowing

When you deposit money in a bank, you are effectively making a loan, for which you get interest in return. Yield farming, also known as yield or liquidity harvesting, involves lending cryptocurrency. In return, you get interest and sometimes fees.

DeFi applications can automatically manage lending and borrowing of assets, acting essentially without any overhead. Furthermore, the logic of calculating interest and risk is fully transparent, with anyone being able to examine the underlying source code.

These income-generating applications are especially attractive to users in the current low- to zero-government-interest-rate environments. Rates of return are considerably higher than traditional assets, going as high as 10% depending on the token.

Examples of popular DeFi lenders are Compound and AAVE.

Decentralized Exchanges (DEXes)

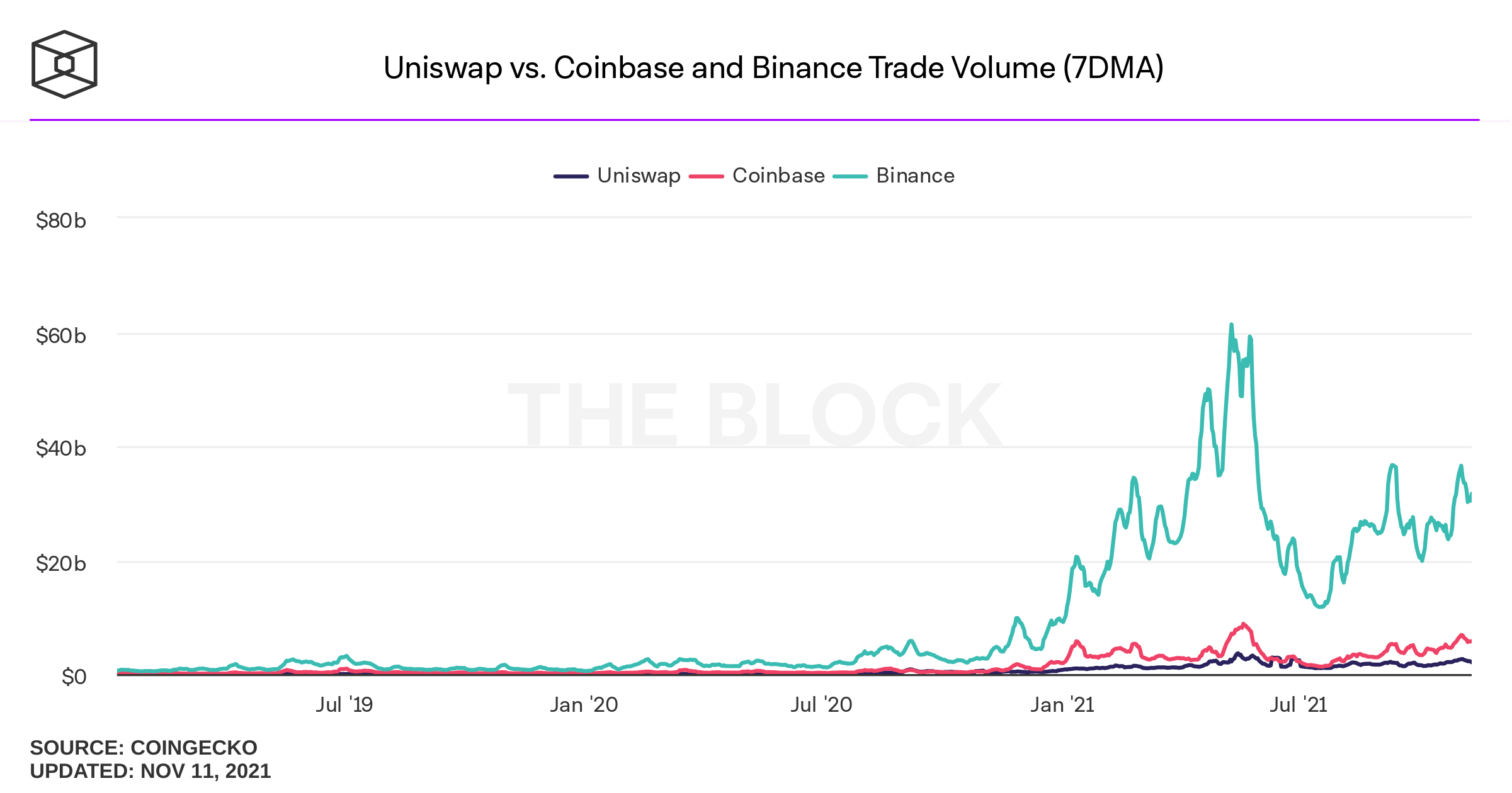

Decentralized exchanges or DEXes are transforming the way crypto assets are traded. There is no central authority on a decentralized exchange to decide who is allowed to trade, or what tokens can be traded. It is a bit like eBay. If you want to sell something, you can list it, in fact Uniswap can be used to trade more than 30,000 different tokens.

DEXs provide trustless efficient peer-to-peer transactions executed by neutral and totally transparent smart contracts. This is in direct contrast to centralized banks and exchanges where central authorities must be trusted even though their inner workings and policies are opaque.

Generally, publicly accessible exchanges use a central limit order book, where buyers and sellers create orders organized by price level that are progressively filled as demand shifts. Exchanges often use market makers to supply liquidity on both sides of the trade.

The Uniswap protocol has no orderbook and uses liquidity pools with liquidity providers who receive pool fees. The price is determined via a mathematical formula that considers supply and demand for a given asset. Its trading volume is approaching that of Coinbase.

Transaction fees on DEXs are much lower than on centralized exchanges where users pay for overhead and administration to central authorities and intermediaries.

Traders manage their own self-hosted wallets and private keys on DEXs, as opposed to on centralized exchanges where they give control to the central organizations.

DEXs do not directly interface with banking systems so it is technically cumbersome to get fiat money into DEXs and it is difficult to move cryptocurrencies from DEX back into bank accounts.

In contrast to centralized exchanges, DEXs do not support any custodial or know-your-customer (KYC) services. This also means users must control their own wallets and private keys when transacting on DEXs. That could raise red flags for government authorities, especially as DEXes gain popularity.

NFTs

NFTs present new ways for content creators to manage, promote and monetize their assets via ecosystems. Entities can depend on the validity, integrity and uniqueness of NFTs.

Outside the art market, NFTs are making inroads into gaming, facilitating in-game asset purchases. Thanks to the implementation of blockchain technology in the gaming industry, you can save in-game purchases, sell them to other players, or move them into other supported games.

Web 3.0

Most of us have primarily experienced the web in its current form. You can think of Web 2.0 as the interactive and social web, defined by large social media companies, providing services to consumers in exchange for their privacy.

Web 2.0 websites and applications are built and deployed to run on a server or store their data in a database, usually hosted on and managed by a cloud provider.

On the other hand, Web 3.0 applications run on blockchains, decentralized networks of many peer-to-peer nodes (servers). These apps are often referred to as dapps (decentralized apps). Compared with traditional internet applications that are based on a centralized server that is a controlling authority for the whole application, dapps use Ethereum-based smart contracts for their application logic. This means no single entity controls the application logic.

Cryptocurrencies play an important role in Web 3.0. It provides a financial incentive (tokens) for anyone who wants to participate in creating, governing, contributing to, or improving one of the projects themselves.

Tokens introduce a native payment layer that is completely borderless and frictionless. Companies like Stripe and PayPal have created billions of dollars of value in enabling electronic payments.

Business Adoption of Blockchain Technology

Business adoption of blockchain technology is lagging compared to public markets. Successful permissioned enterprise blockchain projects are scarce. This is most likely due lack of data privacy controls required for most enterprise applications and a shortage of skilled talent to implement solutions.

The long-term view remains that blockchain will have deeply transformative effects in the enterprise, increasing efficiency, resilience and driving down costs.

Taking a broad look across industries it is easy to see opportunities for disrupting intermediaries using blockchain.

|

Securities

Post-trade

settlement Derivative

contracts Securities

issuance Collateral management |

Retail

Banking Lending Cross border

remittances Mortgage contracts |

|

Trade

Finance Bill of

Lading Cross-currency

payment Intra-bank settlement |

Public

Records Real estate

records Vehicle

registrations Business

license and ownership records Art provenance |

|

Manufacturing |

Legal |