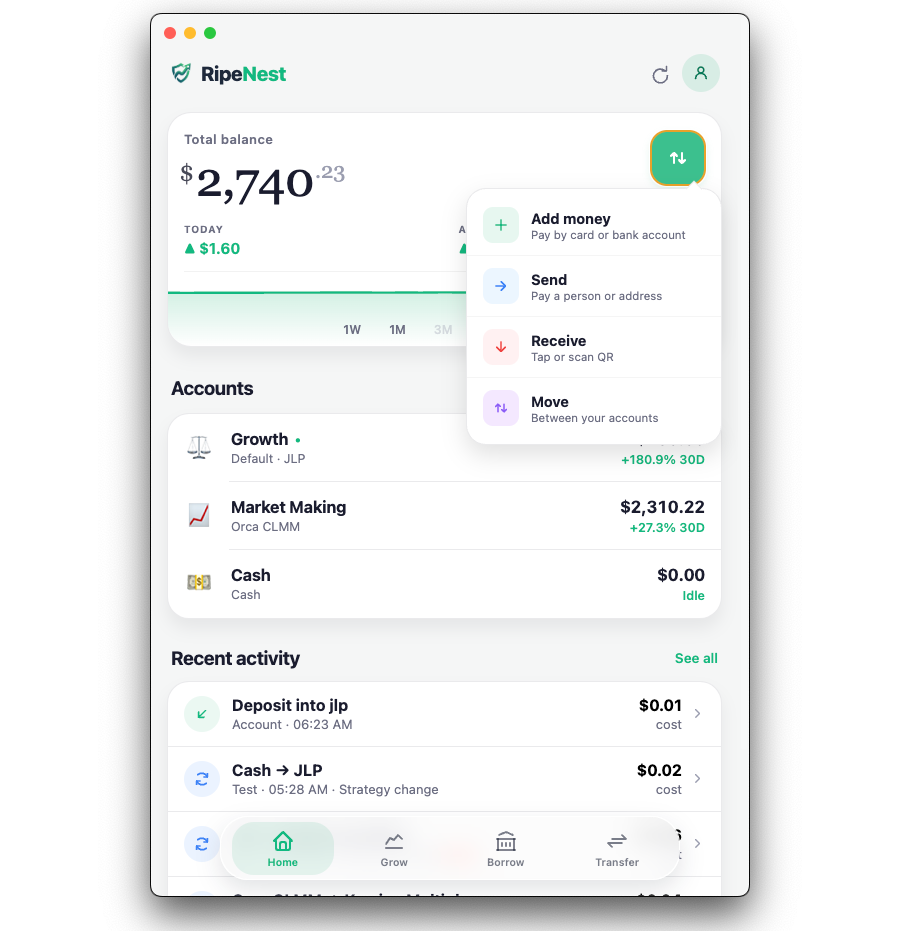

I Built a Stablecoin Wallet that Earns 20% Yield

I set out to reconstruct a consumer banking experience on the blockchain. By taking a USD-first approach and keeping decentralized infrastructure behind the scenes, the app feels remarkably ordinary. It delivers frictionless payments, stable balances, and self-custody—mirroring everyday banking.

For years, I shared the prevailing view among incumbents that the crypto market was structurally immature. The heuristic was that they imitated the surface-level functions of financial services companies while fundamentally lacking its rigorous, systemic substance. To meaningfully test this hypothesis, I took a hand-on approach: I set out to reconstruct a core consumer banking experience using open, blockchain infrastructure. The excitement around stablecoins made me genuinely interested in taking a deep dive.

Rather than settling for a proof-of-concept, I built an application focused entirely on everyday usability. To make the experience as intuitive as traditional banking, I prioritized stable dollar balances, mobile self-custody, and text-message-simple P2P payments, alongside in-person merchant acceptance, competitive yields, borrowing capabilities, and seamless fiat on-ramps.

The resulting application feels entirely ordinary to the end user, yet it operates exclusively on decentralized ledgers, completely bypassing centralized financial infrastructure.

Banking on the Blockchain

Custody. For centuries, keeping money safe meant physical security: a bank's vault, armored trucks, guards, a ledger locked in a back office. The blockchain replaces all of it with math. Instead of one fortified building that thieves can rob or authorities can seize, the ledger is copied across millions of machines worldwide, there's no single door to break down, and no quiet way to rewrite what it says. A bank protects your money by guarding the place it's kept; the blockchain protects it by making the record impossible to forge. You claim your wallet with a private key, backed up to a protected iCloud vault, so losing your phone doesn't mean losing your money.

A stable unit of account. A vault only helps if its contents hold value, and for years crypto failed this, an asset that moves 15% before lunch can't price a coffee. Stablecoins changed that: a dollar-pegged token behaves, most of the time, like a dollar. The app denominates everything in those dollars, so the user never chooses between USDC and USDT.

Payments. A bank takes time to clear an IOU because the two parties sit on two ledgers, reconciled over days through correspondent intermediaries. On a blockchain they share one ledger, so payment and settlement become a single atomic event — clearing in seconds, at a cost floored near a fraction of a cent. This is the most unambiguous win, and largest in cross-border payments, where legacy rails bleed days and whole percentage points to FX spreads and intermediaries (wires run 2–7%; average remittances ~6.5%, versus 0.1–0.5% on-chain). Which is why every major processor now has a stablecoin effort.

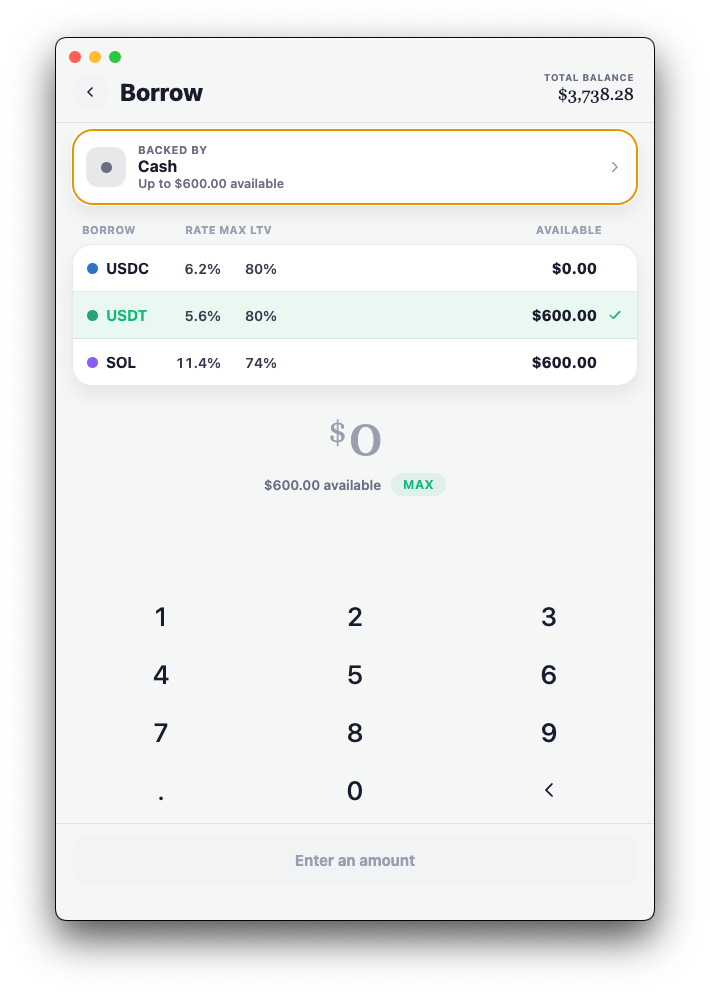

Credit. A bank lends idle deposits at a spread, the origin of interest. On-chain, that market exists with the intermediary removed: you supply dollars, a borrower posts collateral, and the spread is set publicly in real time. Real, with novel but manageable risks.

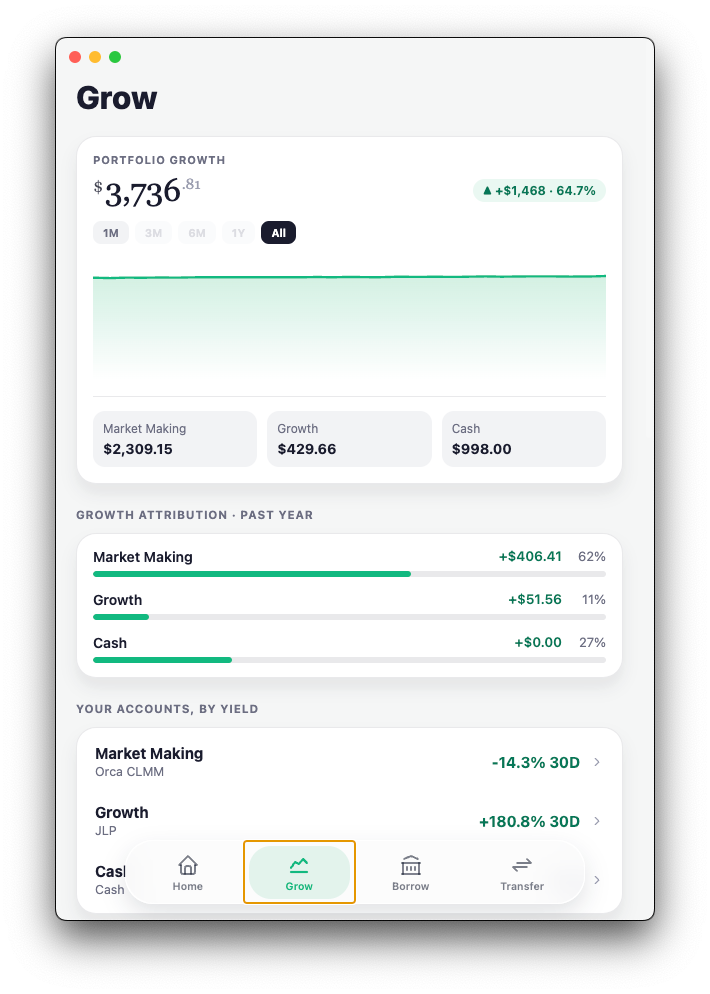

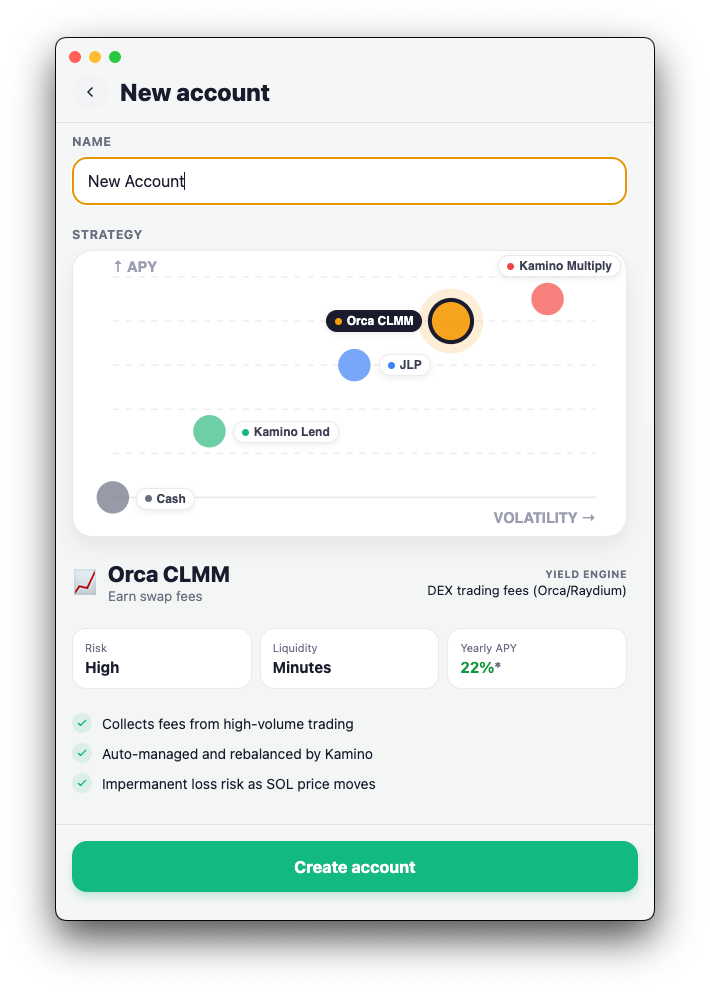

Yield

1. Tokenized Treasuries. Funds like BlackRock's BUIDL and Ondo's USDY are backed one-for-one by short-dated Treasuries, held by regulated custodians, now running on Solana at roughly 4–5%. This is the on-chain risk-free rate, the same T-bill, in the same wallet, and the baseline every higher tier is measured against.

2. Supplying dollars. USDC supplied to Kamino pays 5–8%, for a structural reason: traders pay real interest to borrow stable dollars for leverage, and you're lending into that demand. No personal liquidation risk; the downsides are two tail risks — a smart-contract exploit or protocol insolvency. That spread is the entire payment for those risks; judge one-to-four points insufficient, and the Treasury tier is the defensible choice.

3. Providing pool liquidity. The next tier, 15–25%, comes from supplying a basket of assets to a pool like JLP and becoming the direct counterparty to traders' bets — taking the house's side. It captures transactional friction and rests on retail speculators' tendency to lose over time. But this is not free carry: you are short the crowd's volatility, collecting a steady trickle and paying out the rare, violent spike. This is an active risk position dressed as passive income, and anyone offering it should say so.

4. Automated market making. The most aggressive tier, 15–35%, carries the bluntest risk. Market makers hold inventory and quote both sides; DeFi makes that a fundable primitive. The app's Growth tier uses Orca, a concentrated-liquidity maker that focuses capital in the active price band, run by Kamino's automated vault. But the physics are harsh: a concentrated maker trades against momentum, so as an asset falls it keeps buying. If SOL fell to zero, the vault would convert every dollar into worthless tokens on the way down. A stablecoin de-peg would do the same in reverse.

You can better understand how automated market making works with this interactive tool:

Drag the price and the band bounds. Liquidity lives only in [Pa, Pb] — fees accrue solely in-range, and price sets your token mix.

Passive Orca LP stops earning when price exits the band (IL stays "impermanent" — recoverable if price returns). Kamino vault auto-recenters to keep earning, but each rebalance turns that IL permanent and pays swap/gas. Illustrative √P model. Orca docs · Kamino ranges & rebalancing

Bottom Line

The technology is impressive where it's strongest: settlement and cross-border payments are meaningfully better, and the "one number" design proves the usability gap is mostly an engineering choice, not something inherent to crypto. Those advances are durable; the serious incumbents are building, not dismissing.

The main friction in crypto is the seam between fiat and the blockchain. While on-chain transactions cost pennies and take seconds, the regulated bridge to an actual bank account remains expensive and slow.

- On-ramps: Cost 3–5.5% via card (pricing in fraud/chargeback risk) or 0–2% via bank transfer (costing 1–3 days in time).

- Off-ramps: Cost 0.5–3%, weighed down by the fragmented patchwork of banking licenses and compliance required to move traditional money.

However, this spread is a sign of immature plumbing, and it is rapidly decreasing. The GENIUS Act secured a clear U.S. regulatory framework for stablecoins, and fiat ramps are now integrating directly with instant-settlement networks like FedNow and SEPA Instant.

The cautions are equally real. Stablecoins can de-peg, smart contracts can be exploited, and protocols can fail. The higher yields compensate for risks that can take everything, as there is no deposit insurance or familiar consumer protections in place. Furthermore, the regulatory perimeter, encompassing money transmission, securities, and disclosure is still being drawn, and this will shape which products survive contact with the mainstream.

My read, as someone at this intersection: this is important infrastructure in an early state, not a finished replacement for banking, and not a passing fad. The right posture is neither evangelism nor reflexive suspicion. Banks spent centuries getting paid to absorb risks their customers couldn't see; this technology brings that risk directly to the customer. And maybe that's the opening worth exploring: a lighter balance sheet, a deeper relationship, and the chance to be the trusted guide for customers, as banks have been historically.

Appendix: Transaction Costs

| Asset / Action | Network fee | Protocol / mint-redeem fee | Slippage $1K–$10K | Slippage $10K–$100K | Slippage $100K–$1M |

|---|---|---|---|---|---|

| Send money (SOL or USDC transfer) | ~$0.0005–0.02 (base 5,000 lamports + optional priority fee) | None | 0 bp | 0 bp | 0 bp |

| Solana (SOL) — swap | ~$0.001–0.02 | DEX pool fee 1–5 bp | ~1–5 bp | ~5–20 bp | ~20–60 bp |

| Tokenized T-bills (Ondo USDY / OUSG, OpenEden TBILL) | ~$0.001–0.02 | Primary mint/redeem: 0 bp fee ($100K min, T+1) + ~25 bp/yr mgmt; Secondary DEX: 1–5 bp | ~5–15 bp | ~10–20 bp | Use primary mint |

| Kamino (lending/vault) | ~$0.001–0.02 | No deposit/withdraw fee; 20–25% performance fee on yield only | ~0 bp | ~0 bp | ~0–15 bp |

| JLP (Jupiter Liquidity Provider) | ~$0.001–0.02 | Dynamic weight-based: ~6 bp base, scales up off-target | ~5–15 bp | ~15–40 bp | ~40–100+ bp |

| Orca (ORCA token / whirlpool) | ~$0.001–0.02 | Whirlpool fee 30 bp typical | ~10–30 bp | ~30–80 bp | ~80–250+ bp |

Based on current mainnet conditions (July 2026)